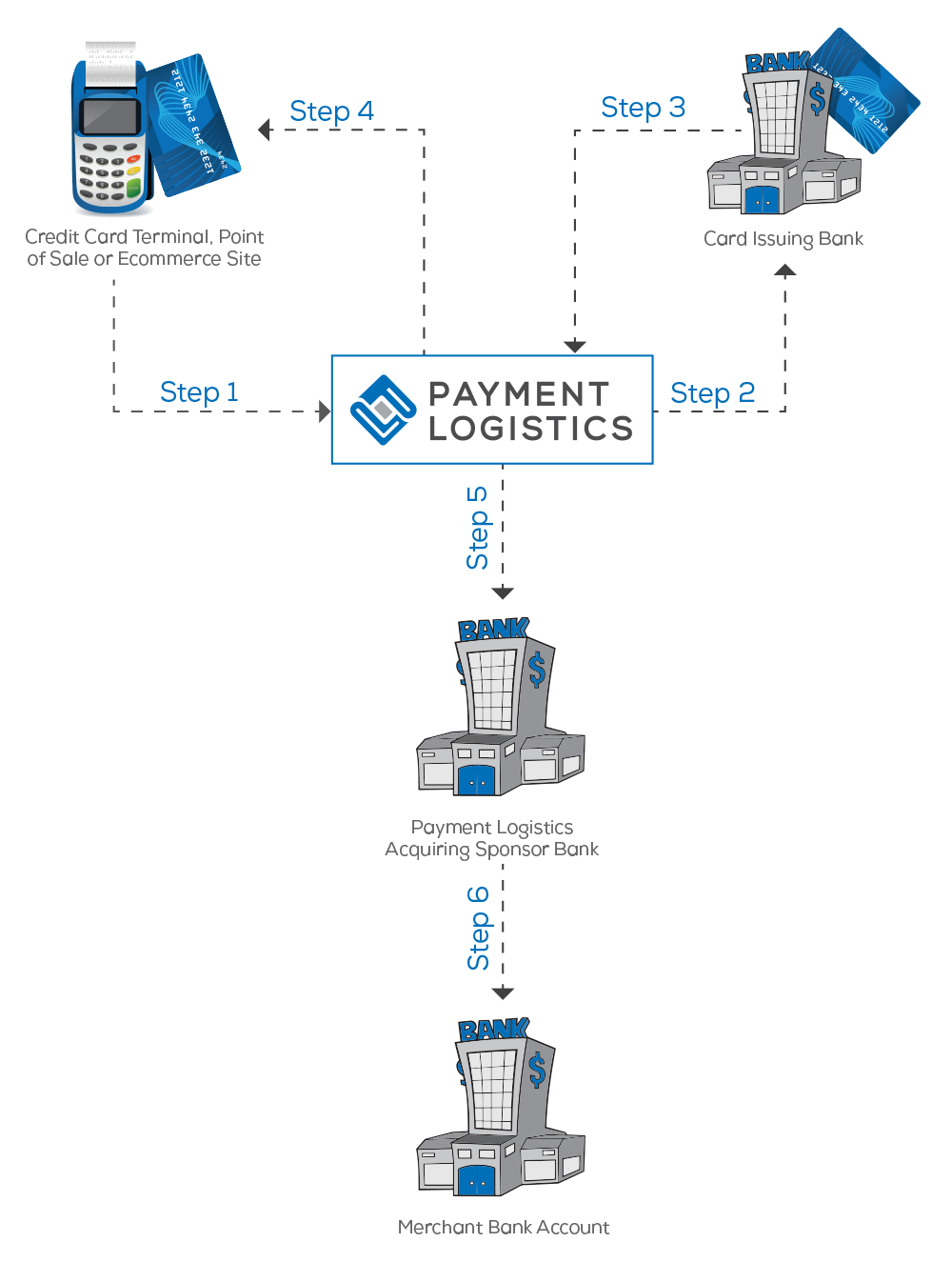

The below diagram and explanation illustrates the steps involved in a typical credit card sale.

Step 1

When your customer makes a purchase, the credit card number is swiped, manually entered or transmitted via a proximity device to the credit card payment device, POS system, virtual terminal or ecommerce shopping cart. The payment device then connects to Payment Logistics for a credit card authorization.

Step 2

Payment Logistics passes the credit card information to the card issuing bank ("CIB") the cardholder is relying on to fund the transaction. The CIB will then perform a verification to determine if the card is valid and if the funds are available on the customer's account. If funds are available, the CIB will temporarily reserve those funds for the merchant requesting them.

Step 3

After the Card Issuing Bank performs its checks it sends Payment Logistics an approval number (authorization code) or a decline message.

Step 4

Payment Logistics then passes the authorization code or decline message back to the credit card payment device. If the charge was approved and depending on how your merchant account is setup, the payment device will print a receipt for the customer to sign. If the charge is declined, the decline message will appear and in some cases provide an explanation for the decline (over the limit, etc.). The entire process from step 1 - 4 takes approximately 12-20 seconds to complete using a "dial up" payment device connected to phone line. Newer Internet or IP based payment devices can cut that time down to about 3 - 8 seconds.

Step 5-6

When your business day is over you must "settle" or "batch out" your payment device to begin the final process of capturing all of your days credit card authorizations. Many payment devices can automatically settle the transactions at a specified time each day, though some payment devices still require a manual "batch out" step. If you are not sure how your payment device works, contact our tech department at 888.624.3687. Once the settlement process is initiated the funds are transferred from the card issuing bank to our acquiring bank in a process called "interchange" and then the final transfer is from our acquiring bank directly to your business checking account through an electronic funds transfer (EFT). Depending on the specific settlement time, you should receive your funds in your bank account 1 or 2 business days after you "batch out".